Electricity Demand and

Generation Capacity Projection

3

Electricity Demand and Generation Capacity Projection

All figures presented in this report correspond to the Mediterranean countries, which include all Med-TSO members plus Bosnia Herzegovina, Malta, and Syria, as shown on the block diagram below. The Mediterranean countries are grouped into four sub-regions: North-West, North-East, South-West, and South-East, as depicted in the following colour coding.

3.1

Electricity consumption perspectives

The following table shows the projected annual electricity consumption for all Mediterranean countries up to 2040 under the three scenarios. The reference year is 2023. The scope of electricity consumption incorporates all uses of electricity (losses included), and new uses such as electric mobility. It also includes the share of consumption satisfied by local production (for example, self-production through rooftop solar panels in the residential sector). However, the electricity demand for electrolysis, which constitutes an energy transformation from electricity to hydrogen, is excluded from the electricity consumption scope.

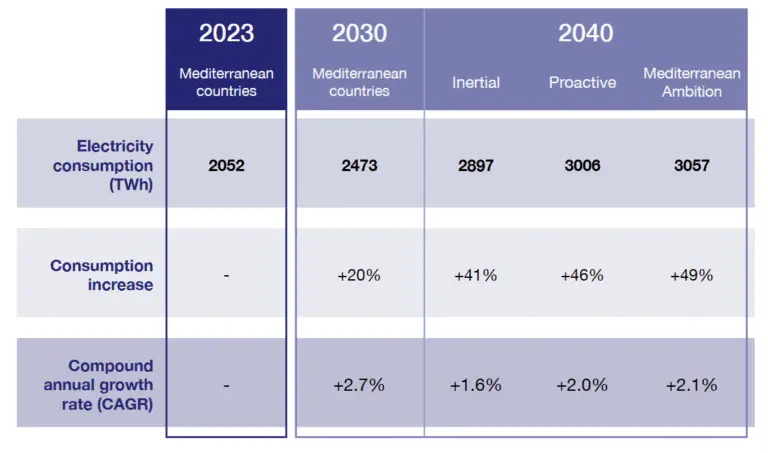

The 2030 projection forecasts an acceleration of the historical growing trend over the current decade, with consumption by 2030 reaching around 2470 TWh, representing an increase of 20% compared to 2023. This corresponds to an average annual growth rate of +2.7%.

By 2040, the electricity demand is estimated to be between 2,900 and 3,060 TWh, depending on the scenario, representing an increase of approximately 40% to 50% compared to the reference year 2023. Over the decade from 2030 to 2040, the average annual growth rate is expected to range from +1.6 to +2.1%. The higher consumption levels in the Proactive and Mediterranean Ambition scenarios, compared to the Inertial scenario, can be explained by a more favourable economic growth assumption (this factor remains the most decisive factor in North Africa, Middle East countries and Türkiye), as well as stronger electrification of the energy sector (mobility, industry, heating processes, etc.).

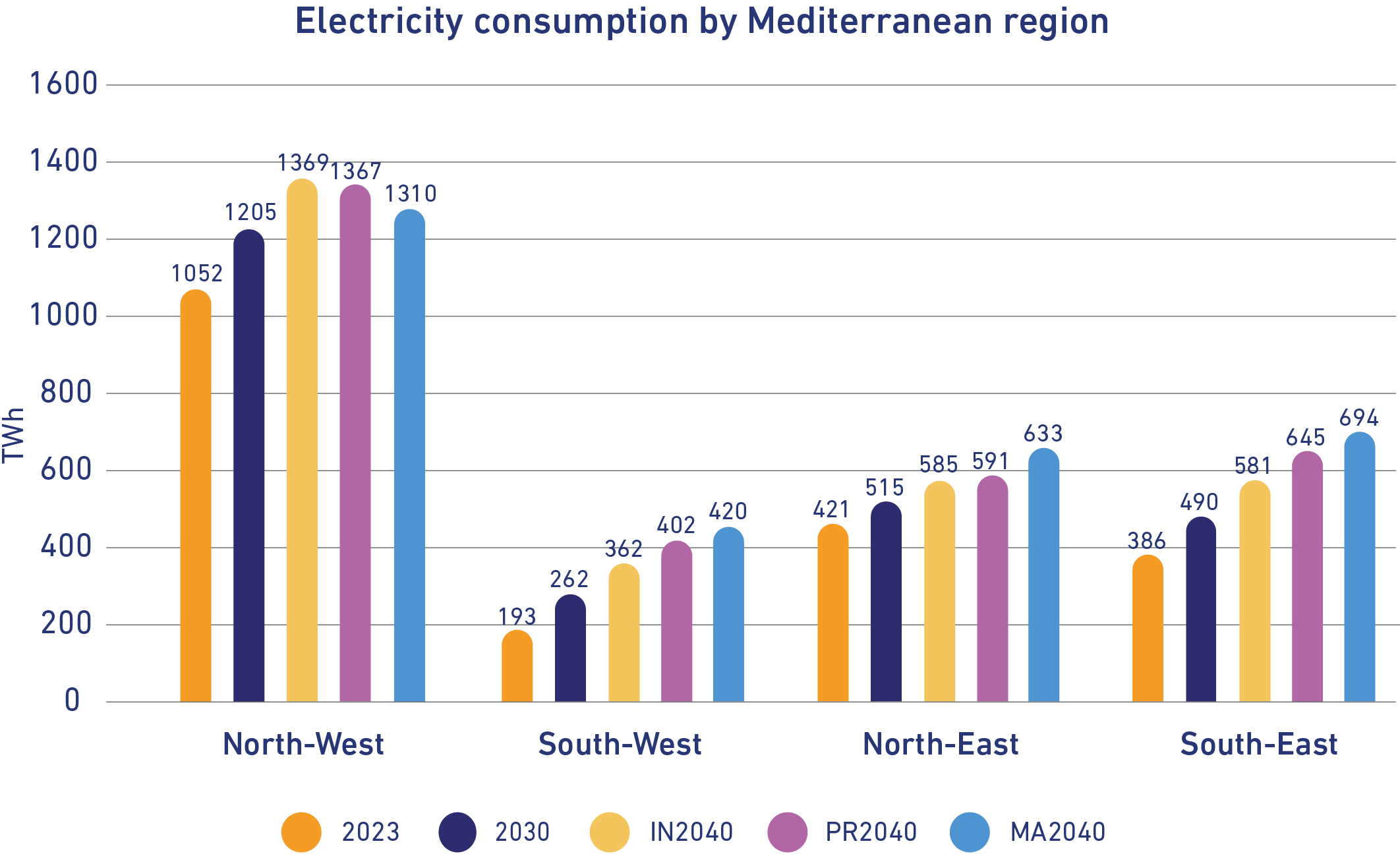

This overall growth includes contrasting dynamics between Mediterranean countries. The evolution of electricity consumption varies significantly among the Mediterranean countries, looking at both the past trends and the 2030 and 2040 outlooks, as illustrated below.

In European countries, particularly the North-West group, the notable growth in direct electrification reflects Europe’s broader strategy to phase out fossil fuels, underscoring the region’s commitment to improving energy efficiency and accelerating decarbonisation (the transportation sector stands out as the primary driver behind the growth in electricity demand).

In MENA countries, the impact of increased electrification is more visible in the Mediterranean Ambition scenario, especially under the assumption of implementing regional cooperation policies across the Mediterranean. Conversely, electricity consumption appears slightly lower in Europe (and some MENA countries) under the Mediterranean Ambition scenario due to increased use of hydrogen, particularly in industry and transportation.

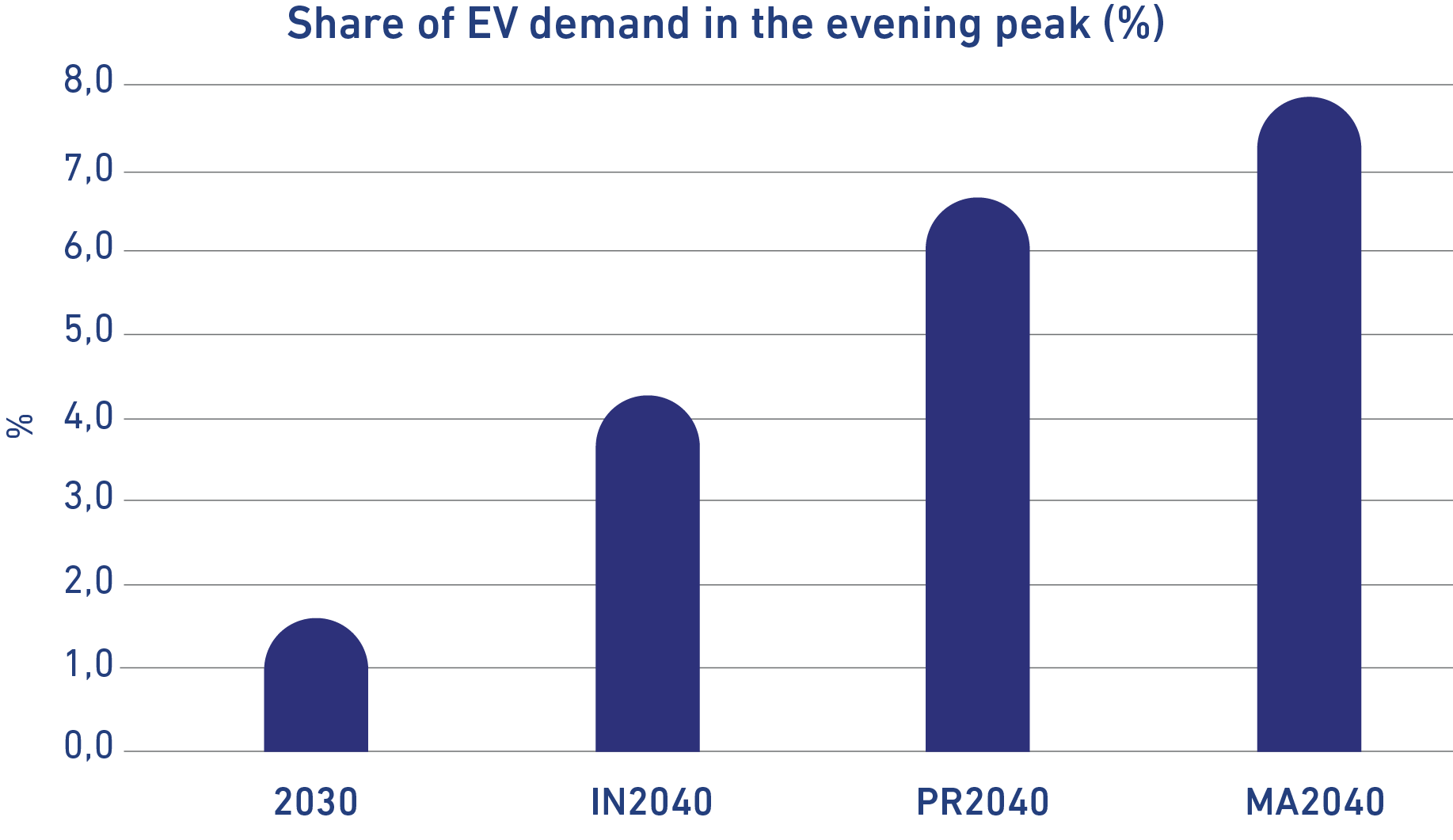

Box 1: Electric vehicle charging demand in MENAT countries

The electric vehicle (EV) fleet in the South-Eastern and South-Western Mediterranean countries remains limited and at an early stage of development. It is not yet considered significant compared to global standards.

However, there is growing momentum and potential for expansion in the future as awareness grows and infrastructure improves.

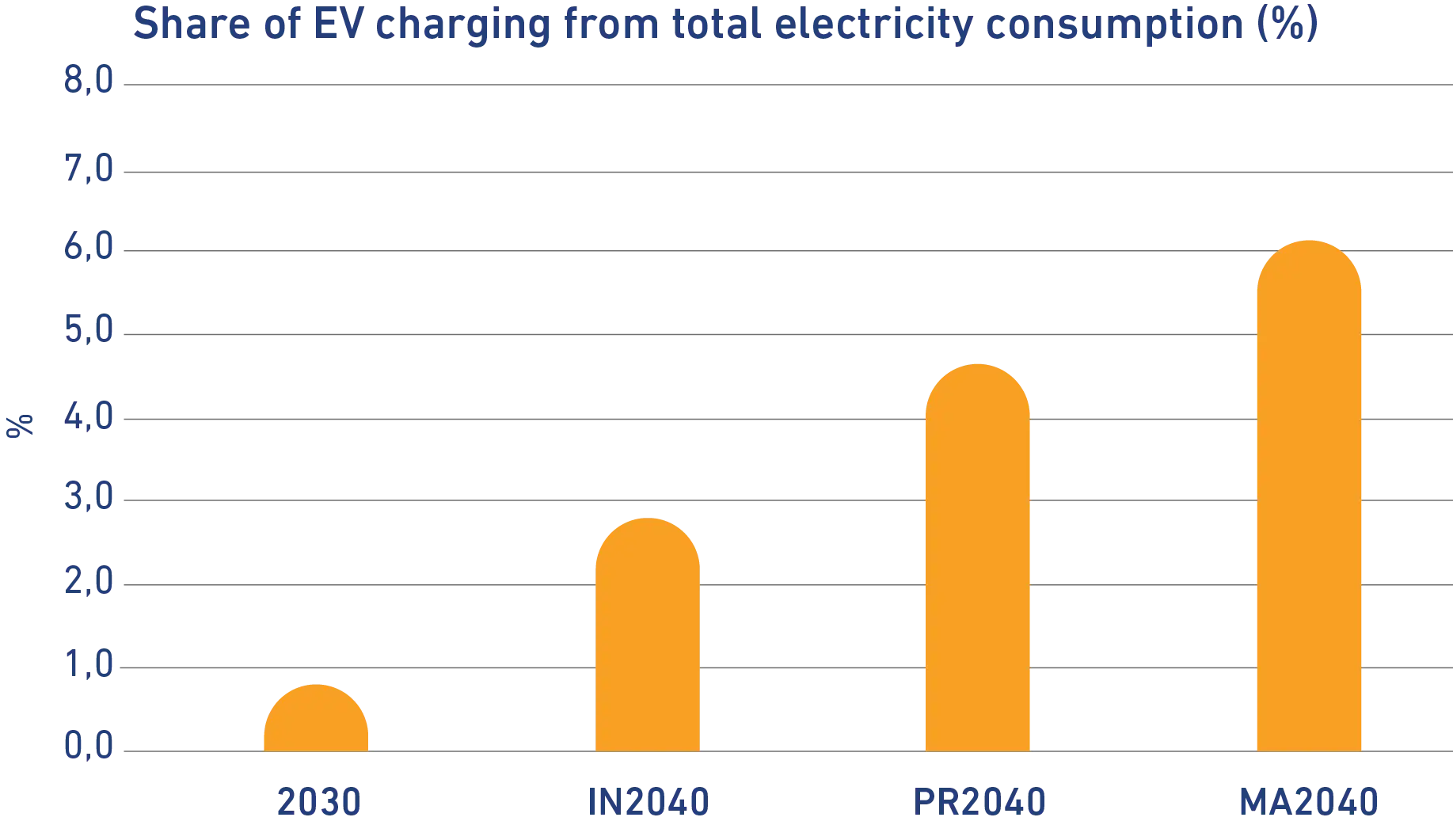

The share of EV charging from total demand is expected to nearly triple from 2030 to 2040. It will represent a major component of evening peak demand, increasing from approximately 1.5% in 2030 to between 4.5% and 8% by 2040. To manage this load effectively and shift EV charging peak load away from the national peak demand periods, countries will need to raise national awareness and apply new regulations, such as Time-of-Use tariffs.

The following two graphs show the share that electric vehicle charging could represent in 2030 and 2040 for all MENAT countries, in annual energy on the left graph, and in contribution to the evening peak consumption power on the right graph.

Graph 6: Share of EV charging in MENAT countries

Generation capacity

In the context of the energy transition, decarbonisation, and electrification of final consumption, power generation facilities in the Mediterranean region will undergo significant changes. The following figure presents the installed generation capacity in 2023, 2030, and according to the three scenarios for 2040, based on the respective primary energy source.

Graph 7: Installed generation capacity in the Mediterranean

This figure illustrates that compared to the reference year 2023, the growth in electricity installed capacity is almost exclusively focused on solar and wind energy. Overall, RES account for 46% of the total installed production capacity (excluding storage capacity) in 2023, with 63% projected in 2030, and between 73% and 79% expected in 2040.

The most significant trend regarding thermal power plants involves the most polluting and CO₂-emitting plants. The cumulative capacity of coal-fired power plants across all Mediterranean countries decreases from 23 GW in 2023 to 14 GW in 2040 (in the three scenarios, with three-quarters of this capacity installed in Türkiye in 2040). Lignite-fired power plants are only marginally present by 2040 (4 GW, solely in the North-East region, Türkiye, and certain Balkan countries).

Gas-fired power plants represent most of the thermal power fleet, and their cumulative installed capacity would remain largely stable (approximately 250 GW) by 2040 across all Mediterranean countries. Specifically, the fleet of gas-fired power plants is significantly decreasing in the North-West region (dropping from about 110 GW in 2023 to 80 GW in 2040), while the rest of the Mediterranean region would see growth in this technology.

The situation regarding nuclear power plants is also varied. By 2030 and 2040, new production sites are planned in Türkiye (approximately 9 GW) and Egypt (nearly 5 GW). In Spain, however, existing plants (approximately 7 GW) are expected to be shut down by 2040 across all three scenarios. For France, the outlook for 2040 remains divergent across the three scenarios (between 50 and 66 GW).

Renewable generation capacity

Of all the electricity generation sectors in all scenarios, renewables account for most of the growth, with remarkable momentum. Indeed, considering all renewable technologies combined, their cumulative capacity for all Mediterranean countries is expected to increase from approximately 330 GW in 2023 to an estimated 630 GW in 2030, and then between 1,030 and 1,370 GW expected in 2040, depending on the scenarios. These figures include renewables specifically dedicated to green hydrogen production.

The figure below presents the outlook for 2040 for the three most developed renewable technologies in the Mediterranean region for electricity production: hydropower, solar, and wind.

With particularly abundant natural resources and already having a strong presence in the region, solar development will continue at a rapid pace due to attractive production costs and seasonality that aligns well with demand. Depending on the scenarios, the installed capacity in 2040 could be four to six times higher than 2023. In North Africa and the Middle East, the equivalent full-load hours for solar range from 1,800 to 2,300 hours and can reach 2,600 hours under the most favourable conditions by using one-axis tracker technology, which is now increasingly deployed in large utility-scale installations.

Installed hydro, wind and solar capacity Mediterranean countries

(in 2030 & TEASIMED scenarios)

Graph 8: Installed hydro, wind and solar capacity in the Mediterranean

Although less impressive than solar, wind development will also continue at a marked pace in the Mediterranean, with an increase in installed capacity by a factor of 3 to 4, depending on the scenarios, by 2040 compared to 2023. In some MENAT countries, wind conditions can be exceptionally favourable for wind development (for example, southern Morocco, eastern Egypt, particularly near the Red Sea, southern Tunisia, etc.), with capacity factors that can reach 50%-60% in certain locations. The figure below indicates the progression of renewable energies across Mediterranean regions.

Total renewable capacity in the Mediterranean regions

Graph 9: Total renewable capacity in the Mediterranean regions

While the Northwest region (France, Italy, Spain, and Portugal) shows the strongest current advancement and the highest prospects for renewable development, the overall trend is well distributed across the entire Mediterranean region. Several other countries have also been engaged in massive renewable development for several years (for example, Türkiye and Morocco), although this trend is more recent for other MENAT countries, as indicated in the following box.

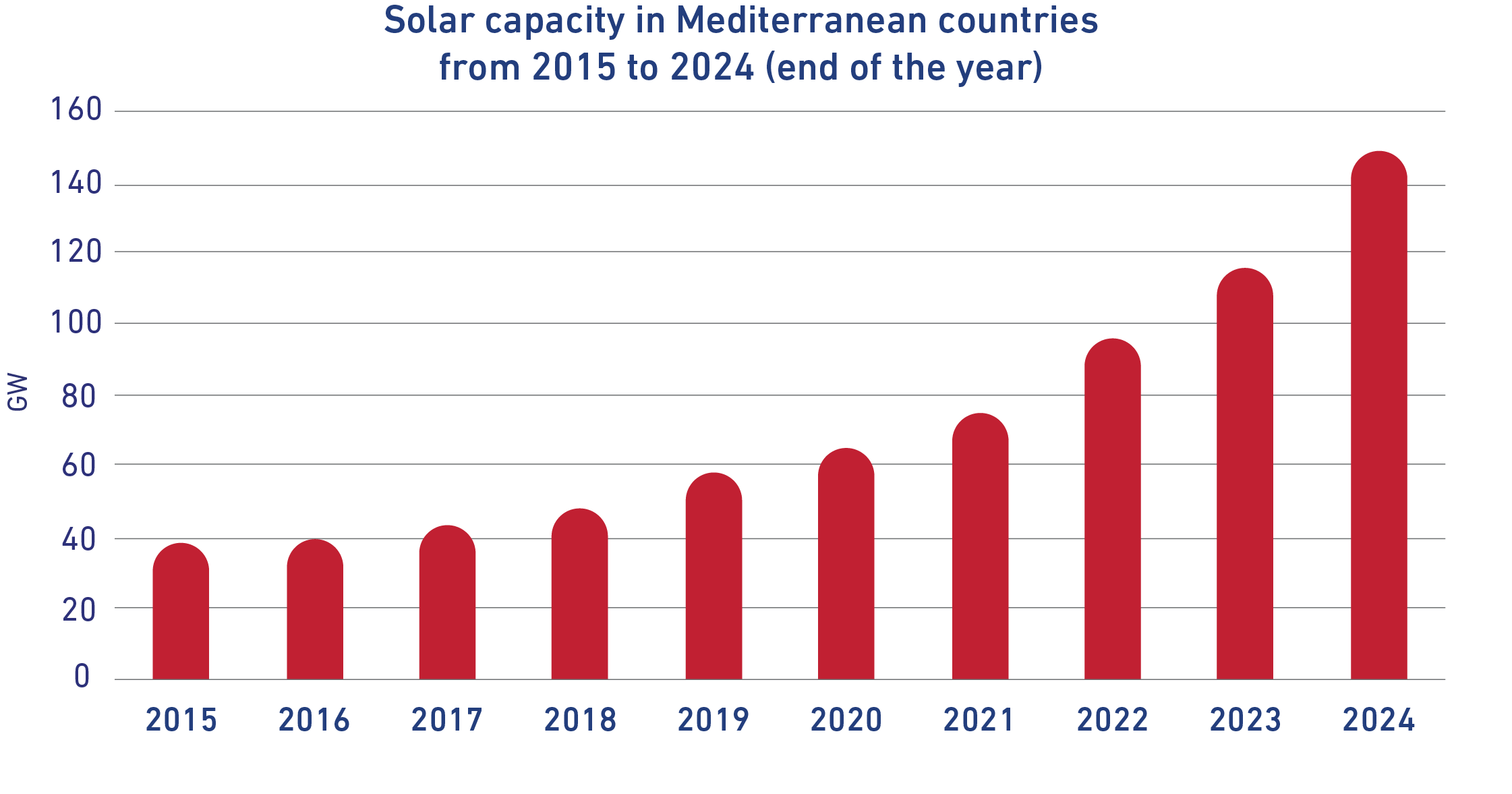

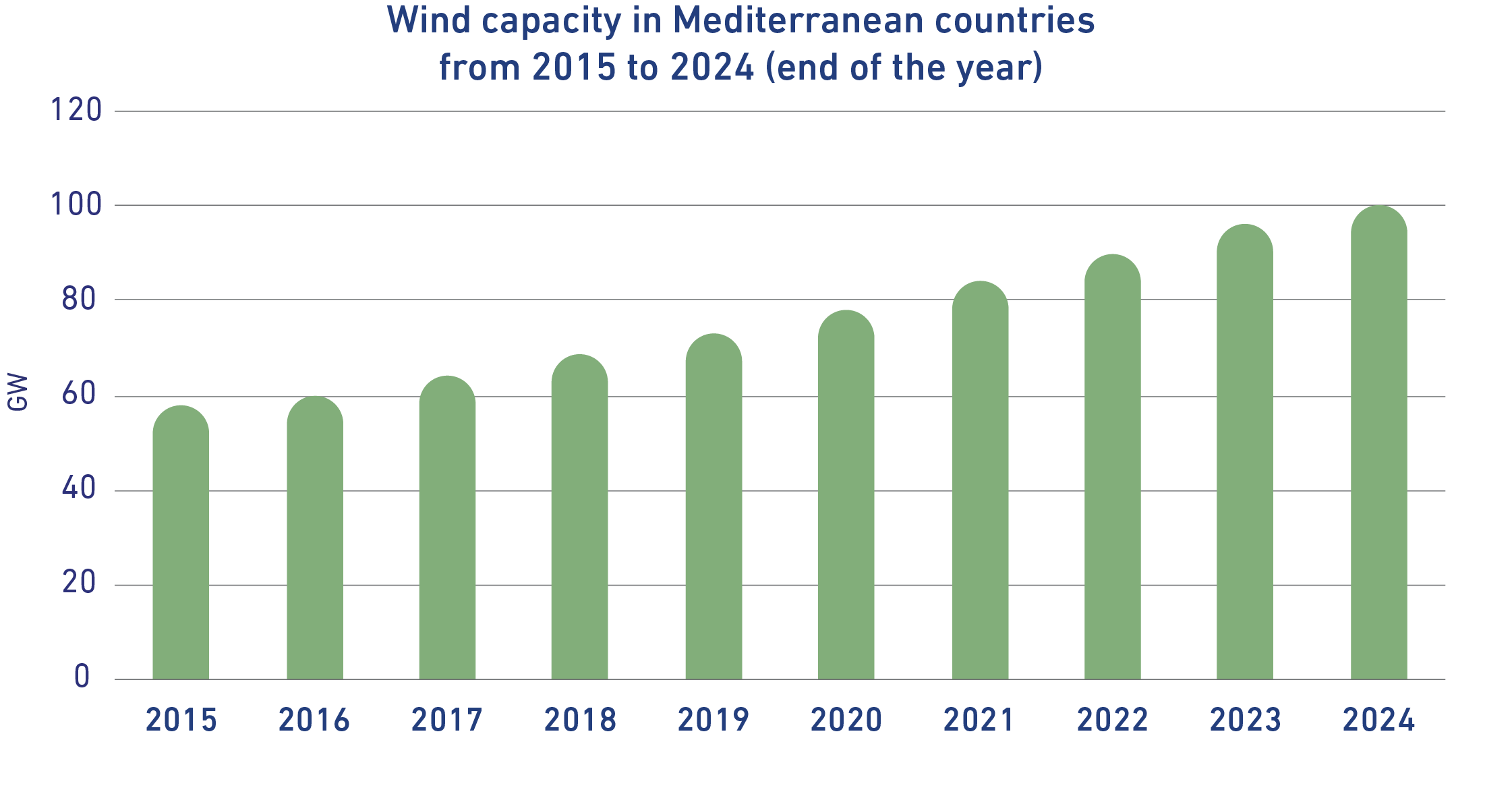

Box 2: Why RES development is anticipated to break from past trends by 2030

The renewable energy share projected for 2030 represents a marked break from past trends, highlighting a deliberate and strategic shift. This transition is driven by several key factors, the foremost being policy acceleration. EU and non-EU Mediterranean countries have increasingly set clear and defined targets for decarbonisation and the transition to sustainable energy systems in their respective national strategies and according to their international commitments under the Conference of the Parties (COP). These frameworks set out clear, defined targets for decarbonisation and the transition to sustainable energy systems. Consequently, achieving these objectives will require a substantial acceleration in the deployment of renewable energy across the region between now and 2030.

Moreover, the continued and notable decline in the costs of solar and wind energy, combined with the increased deployment of battery storage, is enhancing the attractiveness and the competitiveness of renewable energy sources relative to fossil fuels. This trend is already evident in the growing number of renewable energy projects currently in the commissioning or tendering stages, as confirmed by feedback from Med-TSO members. Further confirmation of this trajectory can be found in the most recent statistics on renewable energy deployment in the Mediterranean, as published in early-2025 by the International Renewable Energy Agency* (IRENA).

Graph 10: Solar and wind installed capacity in Mediterranean countries from 2015 to 2024

Considering the most recent trends and observed progress, the 2030 targets for installed solar energy capacity appear to be achievable at the current pace. However, meeting the corresponding targets for wind energy deployment will require increased efforts and accelerated action in the coming few years.

Box 3: Zoom in on dedicated RES for green hydrogen production in North Africa

Most MENAT countries have published roadmaps and/or national strategy documents in recent years, focused on production of renewable hydrogen and its derivatives for domestic and global markets, leveraging their cost-effective and abundant wind and solar resources.

Thanks to the most favourable renewable resources, as well as industrial synergies and opportunities (particularly in the fertiliser sector), the highest ambitions for green hydrogen production are held by Morocco, Tunisia, and Egypt.

The graph below presents the development prospects for solar and wind capacities across North African countries. It distinguishes, on the left side of the graph in dark colours, renewables not dedicated to hydrogen (also known as shared RES), and on the right side in light colours, renewables specifically dedicated to green hydrogen production

Graph 11: Shared and dedicated wind and solar capacity in North Africa

The development of the renewable capacities dedicated to renewable hydrogen production is expected to emerge mainly after 2030, primarily in the Mediterranean Ambition scenario due to ambitious prospects for international cooperation.

This graph clearly illustrates that the development of renewables dedicated to green hydrogen does not hinder the overall development of renewables associated with the decarbonisation of the electricity production sector, thereby aligning with the European regulation and the spirit of the additionality principle. On the contrary, the green hydrogen sector enables a doubling, or even more, of renewable capacities in the Mediterranean Ambition scenario, potentially reaching 300 GW by 2040 in North Africa.